Akila is an Open Banking concept built for the new digital user — the millennial who wants transparency, privacy, and control over their financial data. A modern alternative to The Big 5.

01 — Overview

During a trip to London, I encountered a digital bank that handled freelance payments from UK clients better than anything I’d seen in Canada. That moment exposed a gap: in the UK, EU, and Australia, banks are required to share customer data securely with apps the customer chooses. In Canada, they aren’t. Akila is the answer to what a Canadian Open Banking experience could look like.

Open Banking is a system where, with the user’s explicit permission, a bank securely shares your financial data with a third-party app through a regulated API — instead of forcing you to hand over your username and password.

Canadians already use this concept everywhere except banking:

That same model — explicit consent, granular permissions, revocable any time — is what Open Banking brings to your chequing account, mortgage, and credit card data.

Without Open Banking, the workaround is screen scraping: budgeting apps and lenders ask for your banking username and password, then log into your bank as you and copy your transactions.

An estimated 9 million Canadians currently share their banking credentials this way — with Mint, Wealthsimple, Koho Earn Interest, and dozens of other apps — because there’s no other option.

It’s the financial equivalent of giving a stranger your house keys to feed your cat. It works, but it’s nobody’s first choice.

The UK banned screen scraping in 2018. The EU did the same. Australia followed in 2020. Canada’s Consumer-Driven Banking Act received Royal Assent in March 2026 — finally bringing the same protections here.

phases — from research to a high-fidelity prototype

global digital banks benchmarked across UX and feature depth

user-controlled data sharing — the core principle of the design

02 — Process

A repeatable framework I follow on every product. Each phase compounds: research informs strategy, strategy shapes wireframes, wireframes become a tested UI.

PHASE 01

PHASE 02

PHASE 03

PHASE 04

PHASE 05

03 — The Problem

In J.D. Power’s 2025 Canada Retail Banking Satisfaction Study, the Big 5 dropped seven points to a satisfaction score of 604/1000. Midsize banks rose five points to 649. The gap is widening every year — and it’s widening on the things millennials and Gen Z care about most: ease of use, personalization, and trust.

Score out of 1,000 · 2021–2025

Source: J.D. Power 2025 Canada Retail Banking Satisfaction Study, n=14,399 retail banking customers.

The 2025 study identifies the friction points specifically: midsize bank customers are far more likely to say it’s easy to review recent transactions (55% vs. 43%), easy to deposit cheques (50% vs. 40%), and to receive information tailored to their needs (78% vs. 65%).

Meanwhile, in the UK and EU, Open Banking has been live since 2018. Customers move, manage, and combine their money across accredited apps using regulated APIs — not by handing over their banking password to whoever asks. Roughly 9 million Canadians still do exactly that today.

Akila was designed for a Canadian Open Banking future that, in 2020, was still hypothetical. The design principles — explicit consent, granular data sharing, no screen scraping — turned out to be the same principles the federal government wrote into law in March 2026.

of Canadians switched their primary bank in the past 12 months — up from 6% the prior three years. Top reasons: poor service, high fees, better promotions elsewhere.

points decline in new account opening satisfaction at the Big 5 in 2025. The frictioned experience starts at sign-up and persists.

The Goal

Build banking that earns trust the way modern products do — with transparency, control, and consent that’s legible at a glance. Not as marketing copy, as actual product behaviour.

04 — Global Benchmarks

In 2020, my original case study scored seven banks against 22 mobile-first features. UK and EU digital banks scored 18–22 out of 22. Canadian options — Tangerine and Simplii — scored 6/22. That was the gap that motivated Akila.

Six years later, the data has changed but the story hasn’t. Below is a refreshed scorecard for 2026 — Canada’s two largest banks (RBC, TD) and its two strongest neobanks (Koho, Neo) measured against Monzo and Revolut on the features that matter most under an Open Banking framework.

05 — Feature Comparison

The Big 5 added analytics dashboards and called it innovation. The features that actually shift control to users — virtual cards, real budget pots, regulated data sharing, free FX — remain the territory of the digital banks that grew up under Open Banking.

| Feature | 🇨🇦RBCRBC | 🇨🇦TDTD | 🇨🇦KKoho | 🇨🇦NNeo | 🇬🇧monzoMonzo | 🇬🇧RRevolut |

|---|---|---|---|---|---|---|

| Open Banking & Data Control | ||||||

| Open Banking ready (regulated APIs) | ✗ | ✗ | ◐early access | ✗ | ✓ | ✓ |

| Granular permissions for third parties | ✗ | ✗ | ✗ | ✗ | ✓ | ✓ |

| Easy transaction export (CSV / data) | ✗ | ✗ | ✓ | ✓ | ✓ | ✓ |

| Mobile-first essentials | ||||||

| Open account in <10 min from phone | ✗ | ✗ | ✓ | ✓ | ✓ | ✓ |

| Real-time spending notifications | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Lock / unlock card in-app | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Virtual / disposable cards | ✗ | ✗ | ✓ | ✗ | ✓ | ✓ |

| Free international card use (no FX fees) | ✗ | ✗ | ◐paid plan only | ✗ | ✓ | ✓ |

| Apple Pay & Google Pay | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Money management & control | ||||||

| True budget pots (move money in & out) | ✗NOMI = analytics | ✗ | ✓ | ✓ | ✓ | ✓ |

| Split bills with contacts | ✓ | ✗ | ✗ | ✗ | ✓ | ✓ |

| Round-up auto-savings | ✗Find & Save = AI sweep | ✗ | ✓ | ✗ | ✓ | ✓ |

| Scheduled recurring payments | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Total score | 5 / 13 | 5 / 13 | 9.5 / 13 | 6 / 13 | 13 / 13 | 13 / 13 |

The takeaway

RBC ties with TD — a bank actively criticized for under-investment in mobile. Adding NOMI marketing and Split with Friends doesn’t close the gap on virtual cards, real pots, regulated data sharing, or free FX. Koho is the only Canadian option approaching parity. The structural gap only closes when the CDBA goes operational in 2026–2027.

Sources: Bank app store listings, Q2 2026 reviews from Hardbacon, NerdWallet, WealthRocket; RBC NOMI & Split with Friends product pages; Koho plan documentation; Monzo and Revolut feature pages.

06 — User Journey

User research is more useful as one specific person than as five blurry ones. Meet Sara — the persona Akila was designed for. Akila is a concept, not a launched product, so this map is hypothetical. But every stage maps to a real friction Canadians face today — and every design decision in the app responds to a moment in this map.

| Age | 28 |

| Background | Freelance graphic designer in Toronto. Banks with TD out of inertia. Uses Wise for international invoices. |

| Insight | Heard about Monzo on Reddit and quietly resents that Canada is missing it. |

← Swipe horizontally to view the full journey →

07 — Security & Trust

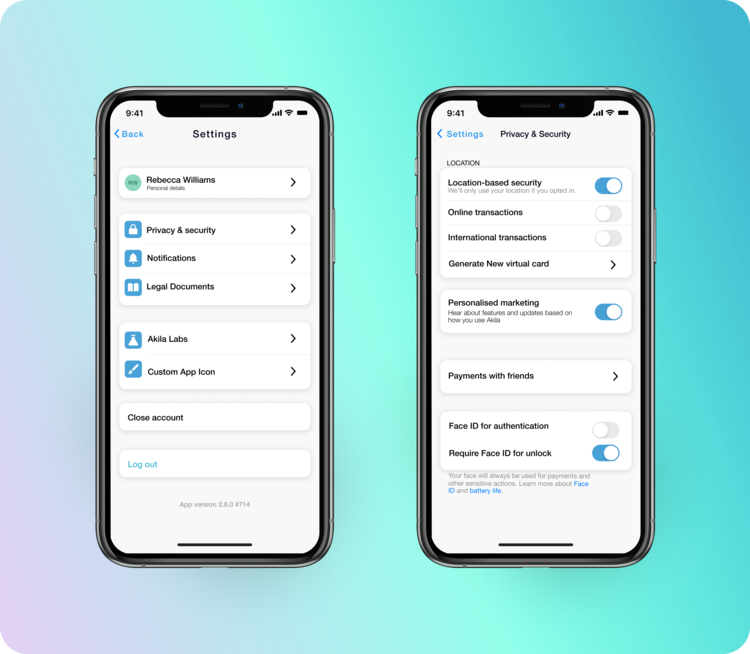

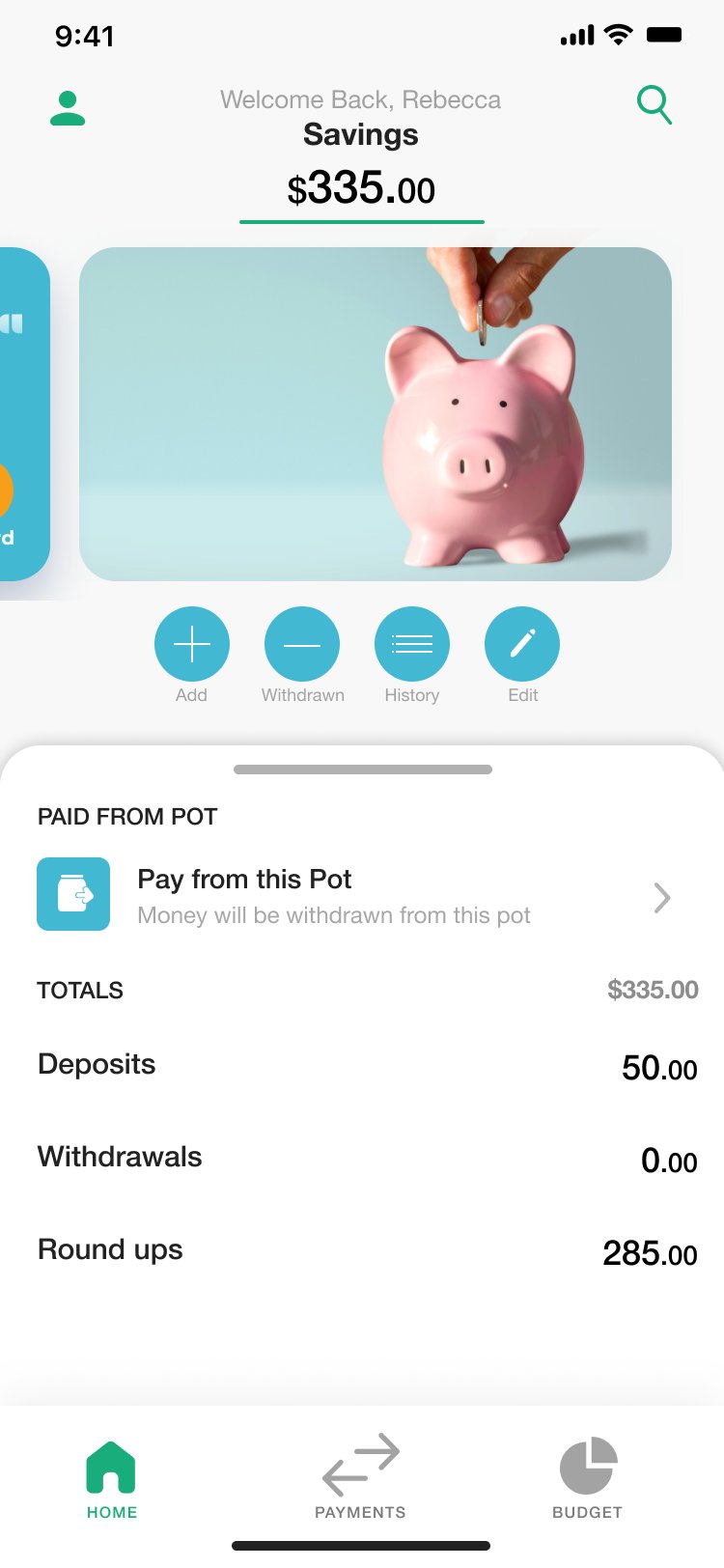

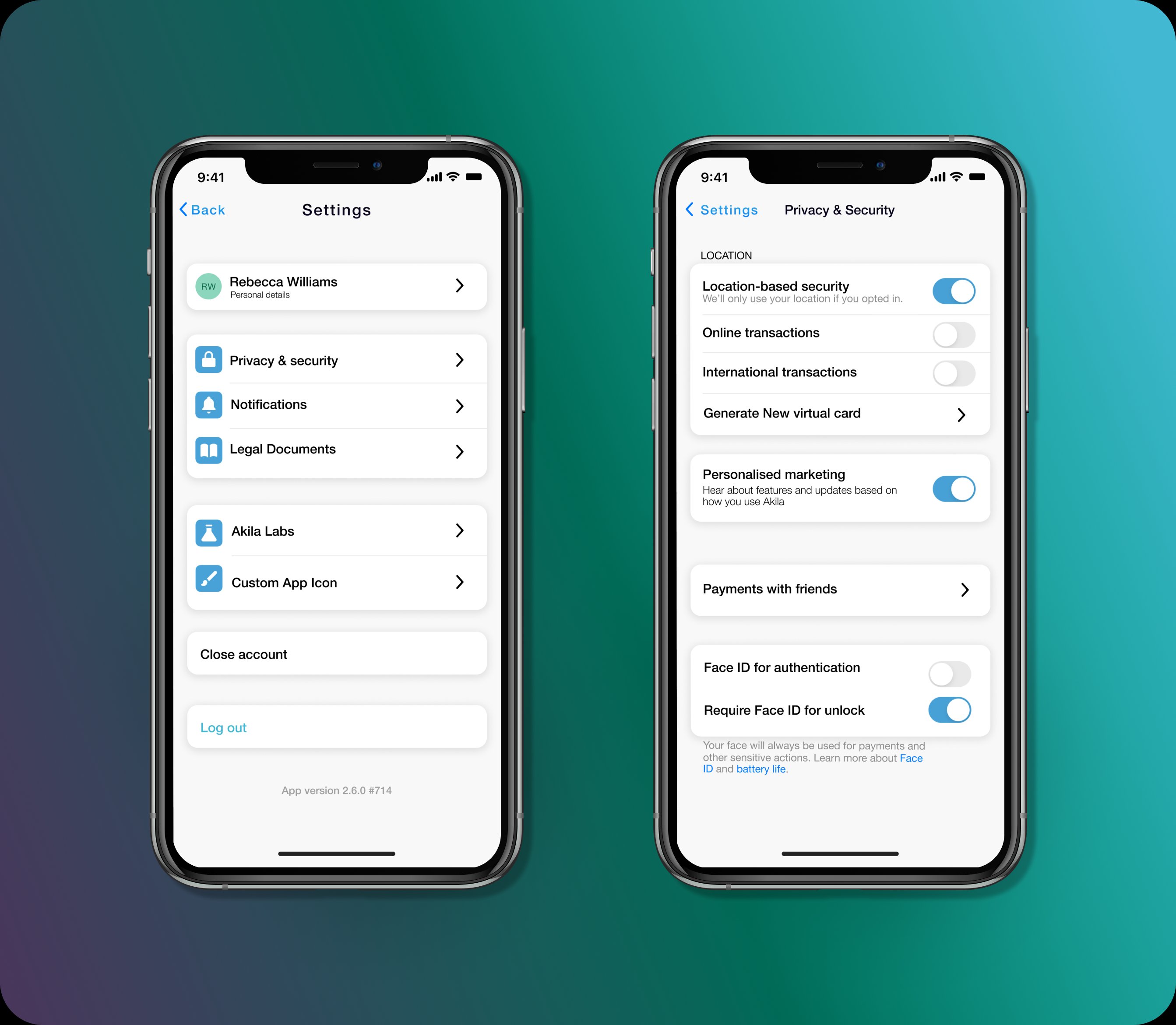

The 2017–2025 wave of digital banks rebuilt fraud protection from the user’s side: granular toggles that let you switch off online payments, contactless, or ATM withdrawals when you don’t need them. Disposable card numbers that regenerate after every purchase. Location-based detection that declines transactions when your phone is in Toronto and your card is suddenly being used in Phoenix. Akila was designed around the same principles — because the actual threat model for a 2026 banking customer isn’t a stolen physical card, it’s a leaked card number from a website breach.

Akila’s permissions screen lets users authorize third-party providers for specific data scopes — and revoke that access at any time. Every permission is explicit, time-bound, and reversible. Users see exactly what data is shared, with whom, and for how long. No buried settings, no quiet renewals.

That’s the design principle. Below is how Canada’s biggest banks compare to UK and EU neobanks on the security controls — the toggles a user actually touches when something feels off.

| Security control | 🇨🇦RBCRBC | 🇨🇦TDTD | 🇨🇦KKoho | 🇨🇦NNeo | 🇬🇧monzoMonzo | 🇬🇧RRevolut |

|---|---|---|---|---|---|---|

| User-controlled toggles | ||||||

| Toggle online / e-commerce payments on/off | ✗ | ✗ | ✗ | ✗ | ◐freeze only | ✓ |

| Toggle contactless / tap-to-pay on/off | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ |

| Toggle ATM withdrawals on/off | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ |

| Toggle international payments on/off | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ |

| Card protection | ||||||

| Disposable / single-use virtual cards | ✗ | ✗ | ◐multi-use only | ✗ | ✓ | ✓ |

| Location-based fraud detection | ✗ | ✗ | ✗ | ✗ | ◐passive only | ✓ |

| Instant card freeze / unfreeze in-app | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Biometric login (Face ID / Touch ID) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Total score | 2 / 8 | 2 / 8 | 2.5 / 8 | 2 / 8 | 4.5 / 8 | 8 / 8 |

What this reveals

Every Canadian option scores 2–2.5 out of 8. Even Monzo, the leading UK neobank, scores 4.5/8. Revolut sits alone at 8/8 because they treated security as a customisable surface, not a black box. The lesson for Akila: the security screen in the design isn’t for showing off encryption badges. It’s for handing users the toggles.

Sources: Revolut Help Center & Safety Features pages (Nov 2025), Monzo Community card-controls discussions, official RBC / TD / Koho / Neo app documentation.

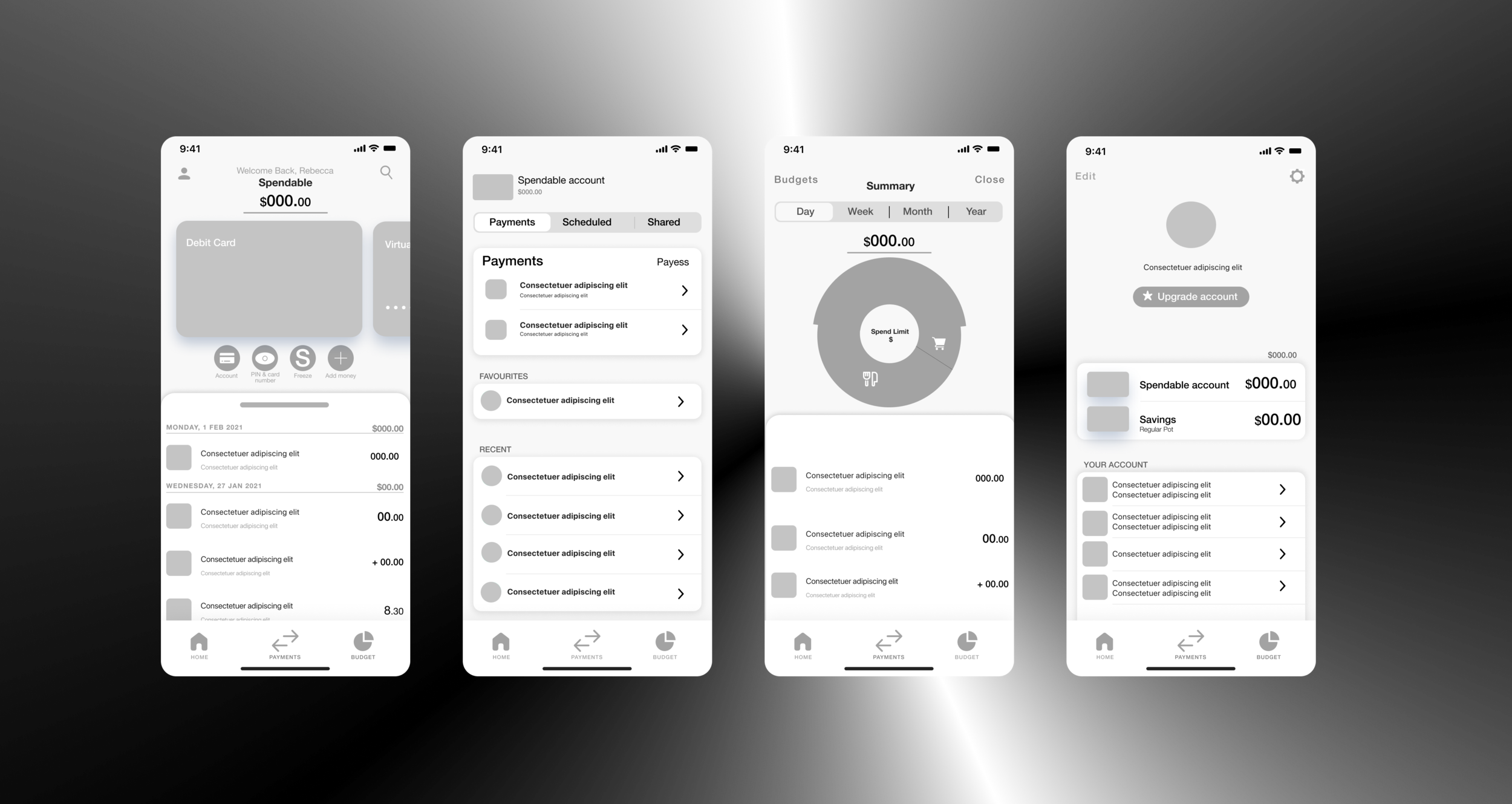

08 — Wireframing

Wireframes focused on three flows that millennials use daily: sending money, tracking spend, and granting/revoking data access.

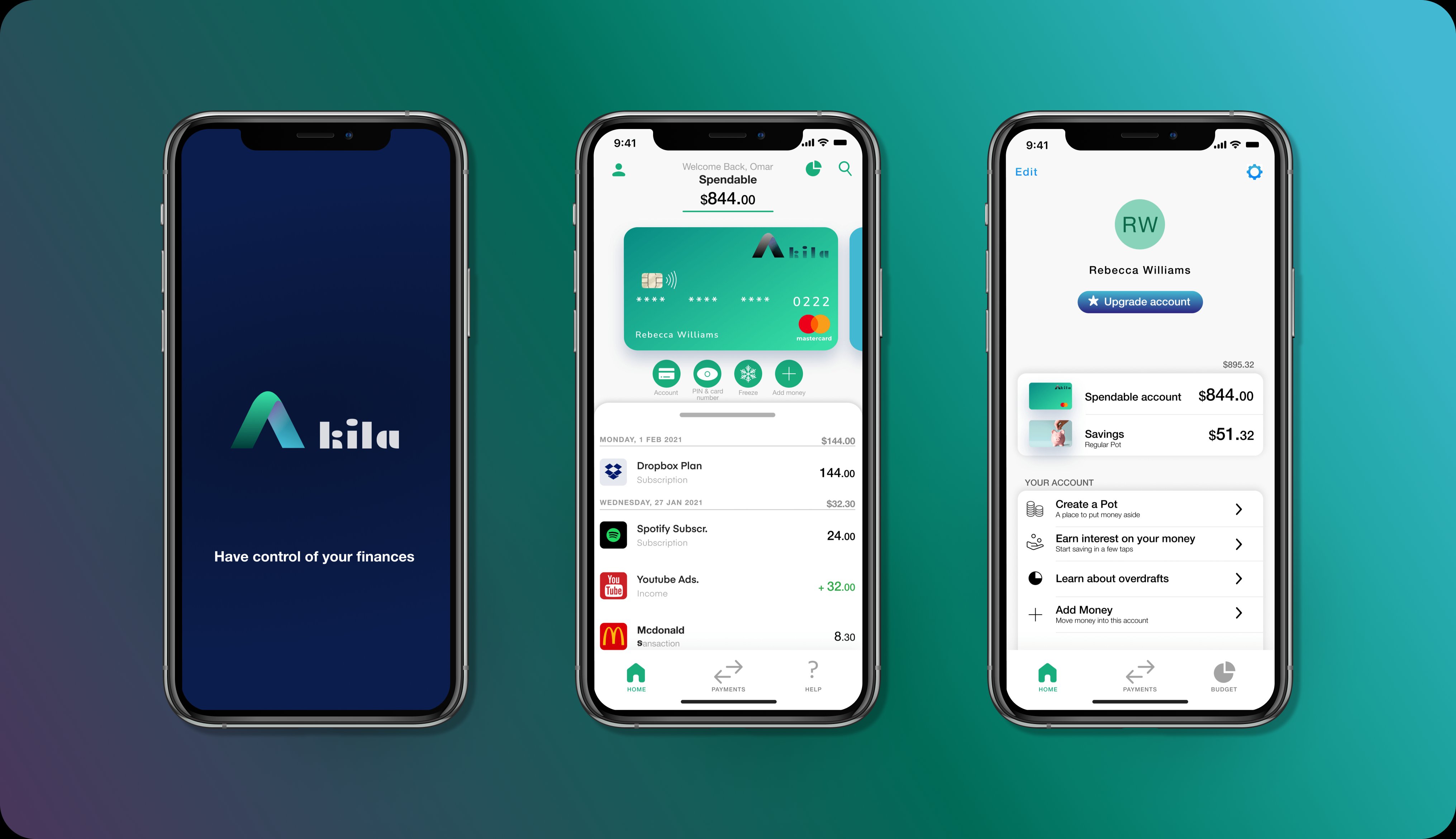

09 — UI Design

A clean visual system built around clarity at glance. Every screen answers one question: what do I need to do, and how confident am I that it’s done?

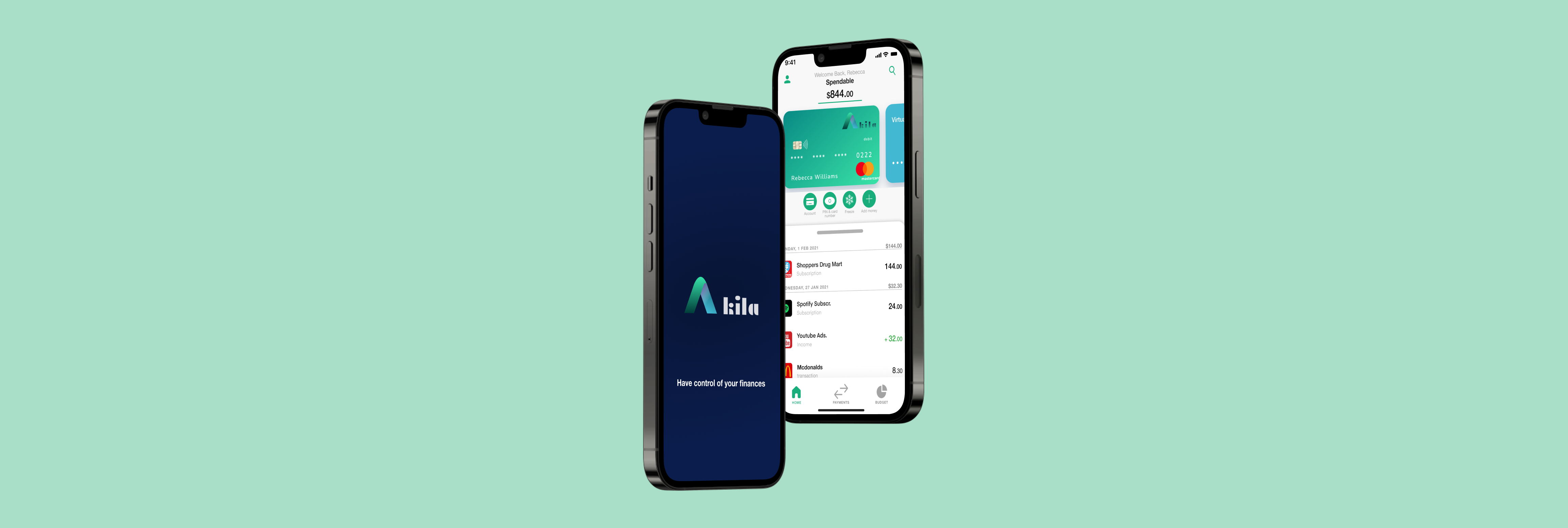

The brand

Onboarding

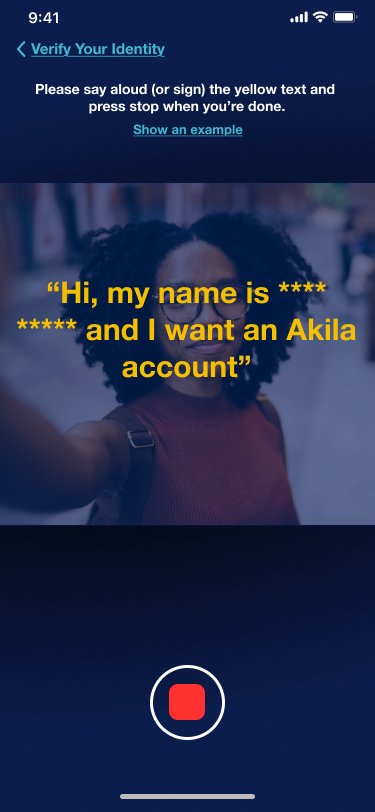

Identity, with consent

The home experience

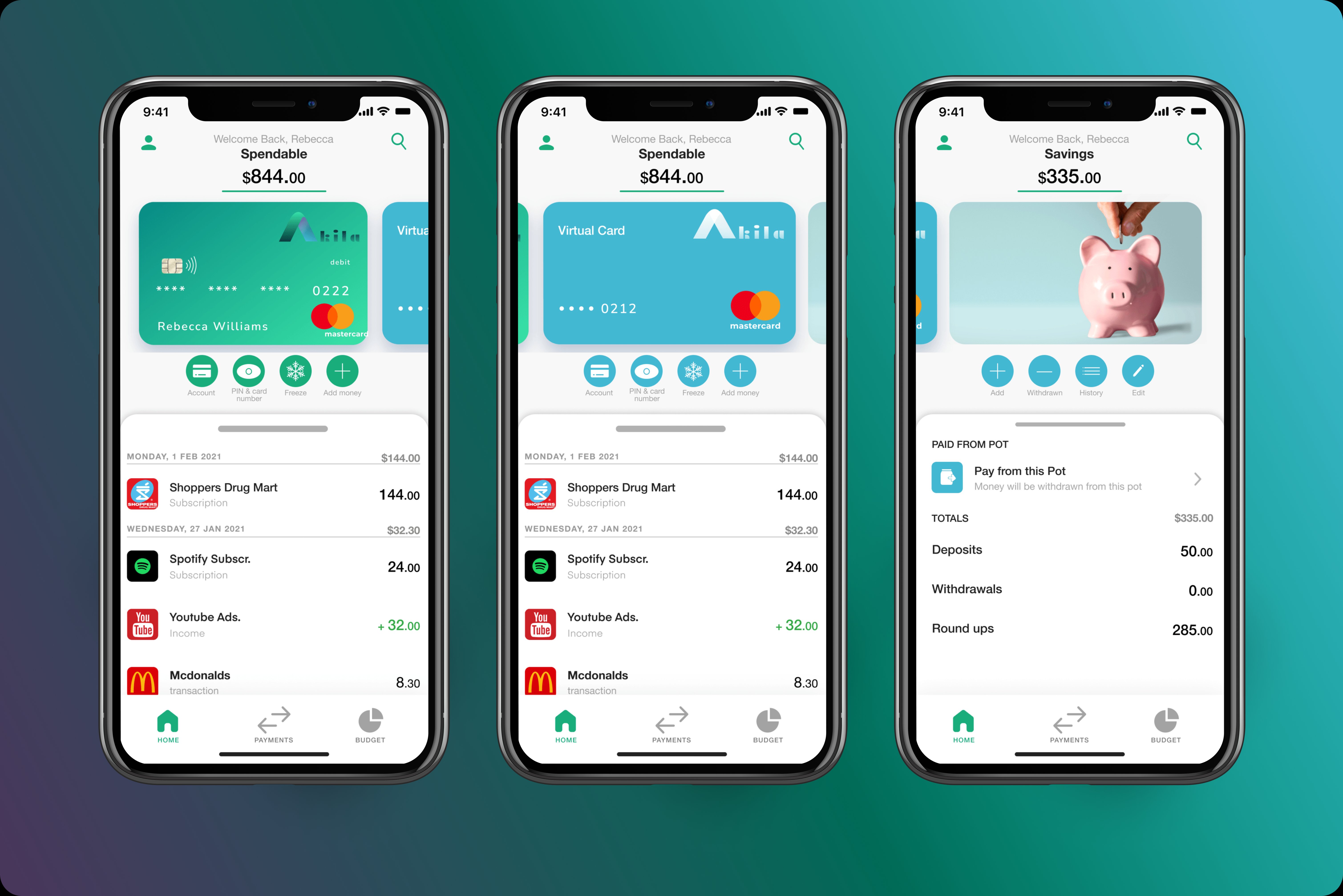

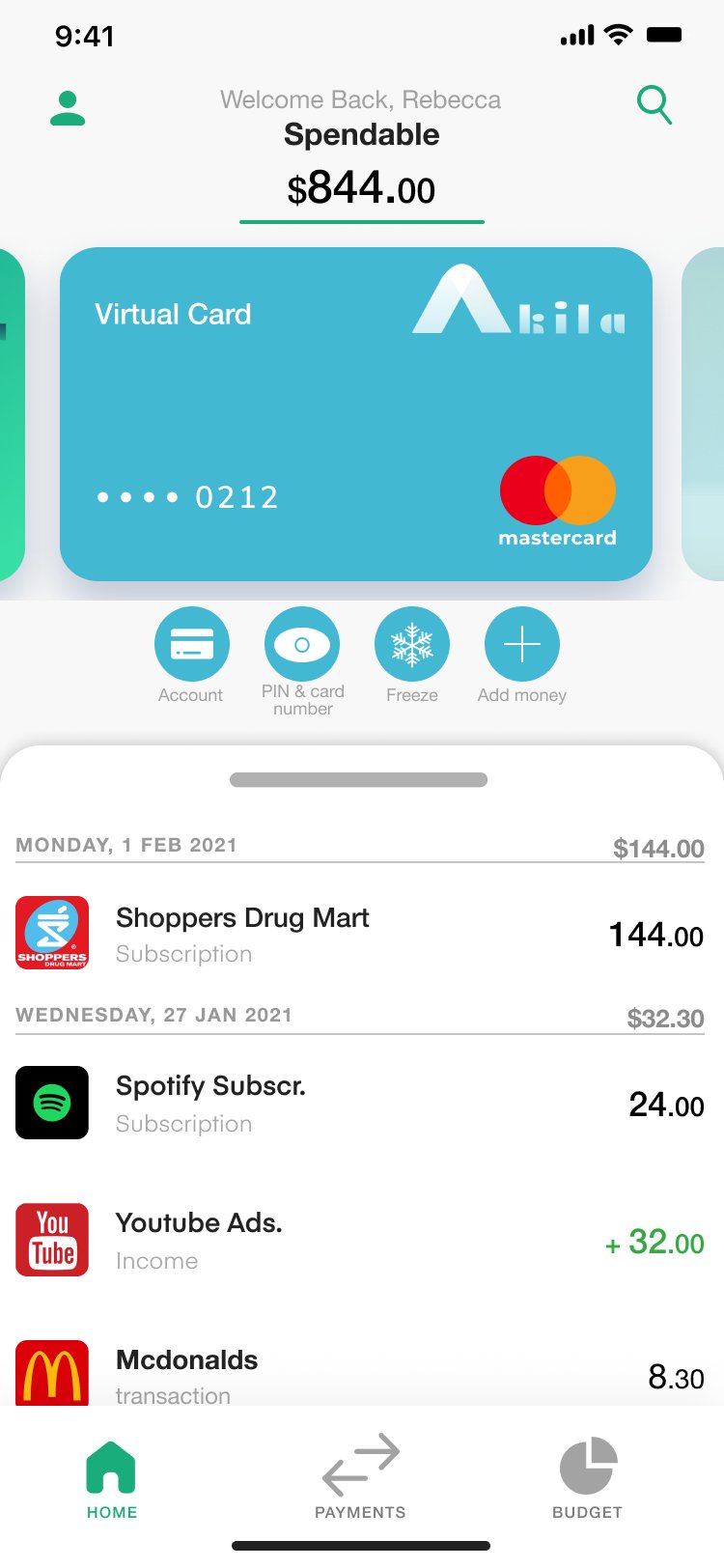

Account types

The features Canada doesn’t have

Budget tracking

Security users actually control

10 — Canada’s Open Banking Timeline

When I designed Akila in 2020, “Canadian Open Banking” meant consultation papers and stalled bills. Six years later, the framework is law. Below is the path Canada actually took — and where Akila fits inside it.

August 2017

The Department of Finance announces it will explore Open Banking. The first of many consultations across the next seven years.

2020

Designed in the gap between the federal consultation papers and the first formal recommendations. The principles came from observing how UK and EU users were already banking under PSD2 — and from research with millennials in Toronto and Vancouver who didn’t know there was an alternative.

April 2021

The committee delivers recommendations for Canada’s framework structure — the same explicit-consent, granular-permissions principles Akila was already designed around. Implementation then stalls in political churn.

June 2024

Royal Assent of the high-level framework. Most of the substantive rules — accreditation, security standards, consent flows — are deferred to future regulations.

November 2025

Budget 2025 shifts oversight from FCAC to the Bank of Canada and confirms the two-phase rollout plan: read access first, then write access.

March 26, 2026

The full Consumer-Driven Banking Act becomes law. Screen scraping is banned. The Big Six must participate. Granular consent is a legal requirement — not a design opinion.

Late 2026 (target)

Accredited fintechs gain regulated API access to consumer banking data. The 9 million Canadians currently sharing passwords get a safer alternative.

Mid-2027 (target)

Payment initiation and account switching land. Contingent on the Real-Time Rail being operational. The point at which a Canadian Akila could actually launch.

What this means

Akila wasn’t prescient — the principles were already proven in the UK and EU since 2018. What it does show is that designing around clear, regulator-shaped principles — explicit consent, time-bound permissions, no password sharing — ages well. The 2020 design didn’t need to be rewritten when the law arrived in 2026.

Sources: Department of Finance Canada Fall Economic Statement 2024, Budget 2025; McMillan LLP regulatory analysis (Nov 2025); Open Banking Tracker country page (Mar 2026); Bill C-15 Royal Assent announcement (Mar 26, 2026).

11 — Takeaway

In 2020, my original case study scored Canadian banks 6/22 on mobile-first features — six years later they’re still scoring 5/13. The features that matter most for trust and control — virtual cards, granular toggles, regulated data sharing — only ship when the regulatory environment forces them. Akila’s design was built around that incoming environment six years before it became law.

What I’d carry forward

Three principles, confirmed by what eventually shipped in CDBA: explicit consent every time — never bury renewals; time-bound, revocable permissions — users own the leash; controls before features — the toggle to switch off online payments matters more than the colour of the card. Designing around these isn’t safer or more conservative. It’s how you build banking that holds up when the law catches up.

Next case study